The ERC, NGCP, inflation and public debt

* My column in BusinessWorld last October 10.

----------------

Four important events that occurred last week: the Energy Regulatory Commission (ERC) dismissed the rate hike petition of the power companies of San Miguel Corp. (SMC); the continuing threat of blackouts was highlighted; the jump in the inflation rate; and, the government’s cash operations and debt payment information were released.

ERC’S DISMISSAL OF SMC POWER COMPANIES PETITION

Last Monday, the ERC published its decision denying the petition of SMC for a rate hike for its two power plants. See these reports in BusinessWorld: “Meralco vows to prevent termination of SMC deals” Oct. 5), “SMC studies legal options after rate hike denial” (Oct. 6), and, “SMC plans to sell power to WESM after rate-hike denial” (Oct. 7).

For me the main issue that the ERC has to grapple with is not the projected higher electricity rate hike if the SMC petition was not granted. The main issue is rule of law and sanctity of contract. If the ERC granted the SMC petition, then it would be a signal for many other generation companies to also go to the ERC and demand a rate hike. Since the rule of law mandates that the law applies equally to unequal people and companies, that no one should grant exception and favoritism, then the ERC would be obliged to also grant those new petitions. A cascade of new generation rate hikes for the consumers would be much larger than the price hike threats of SMC.

The ERC made the correct decision. Thank you, ERC, for doing your job and protecting the consumers...

BIG JUMP IN INFLATION RATES

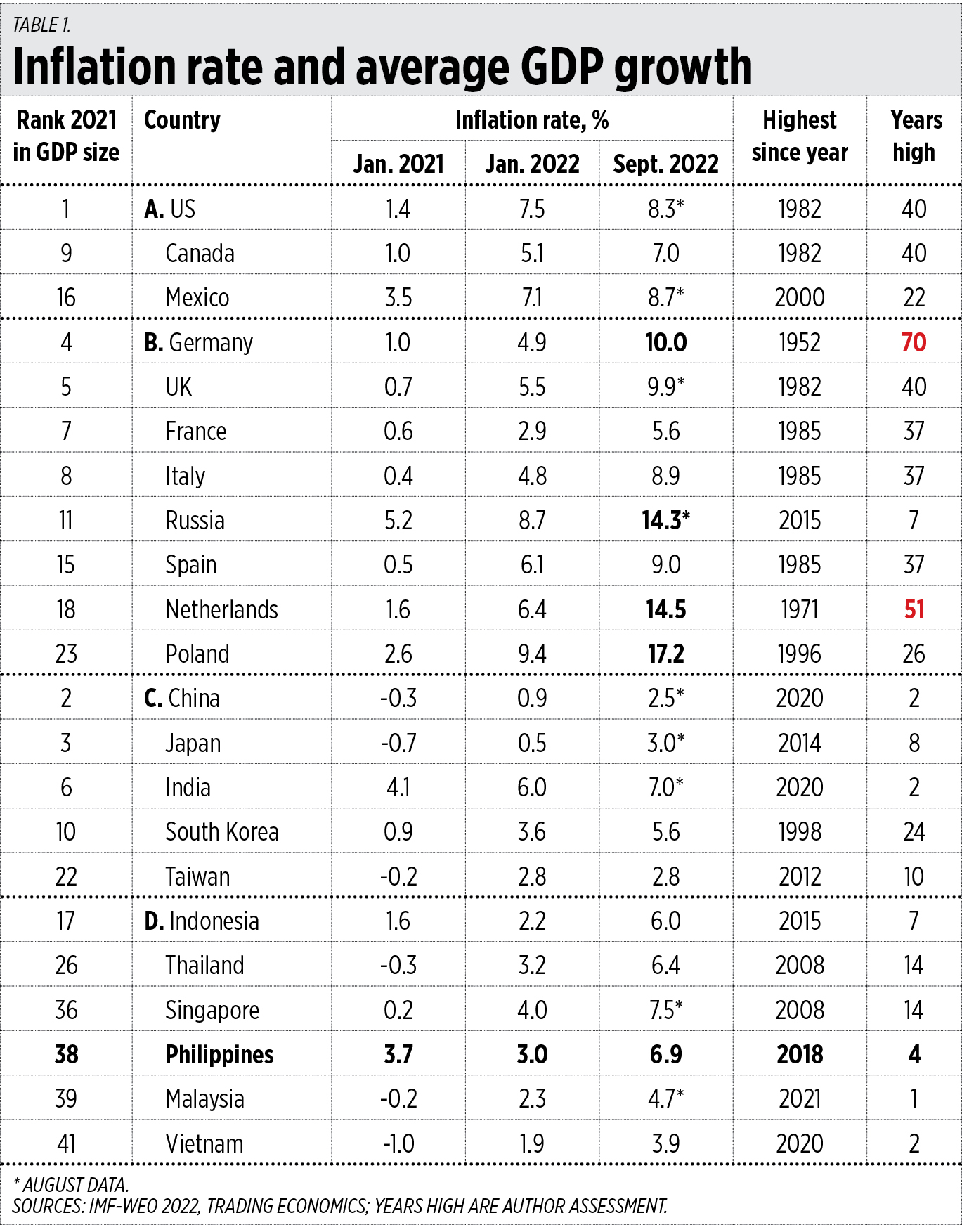

Last week, the Philippine Statistics Authority reported the September inflation rate at 6.9%, up from August’s 6.3%. This is indeed high but is still only a four-years high compared to Germany’s 70-years high, the Netherlands’ 51-years high, the US, Canada, and the UK’s 40-years high, and France, Italy, and Spain’s 37-years high (Table 1).

The 6.9% inflation rate was used by some bashers of the Marcos Jr. administration and its economic team’s performance. This is misplaced criticism. One, our four-years high in inflation is among the more benign levels in Asia and the world’s large economies as shown in the table. Two, no price control was imposed, especially on oil products.

DOF-DBM CASH OPERATIONS AND DEBT PAYMENT

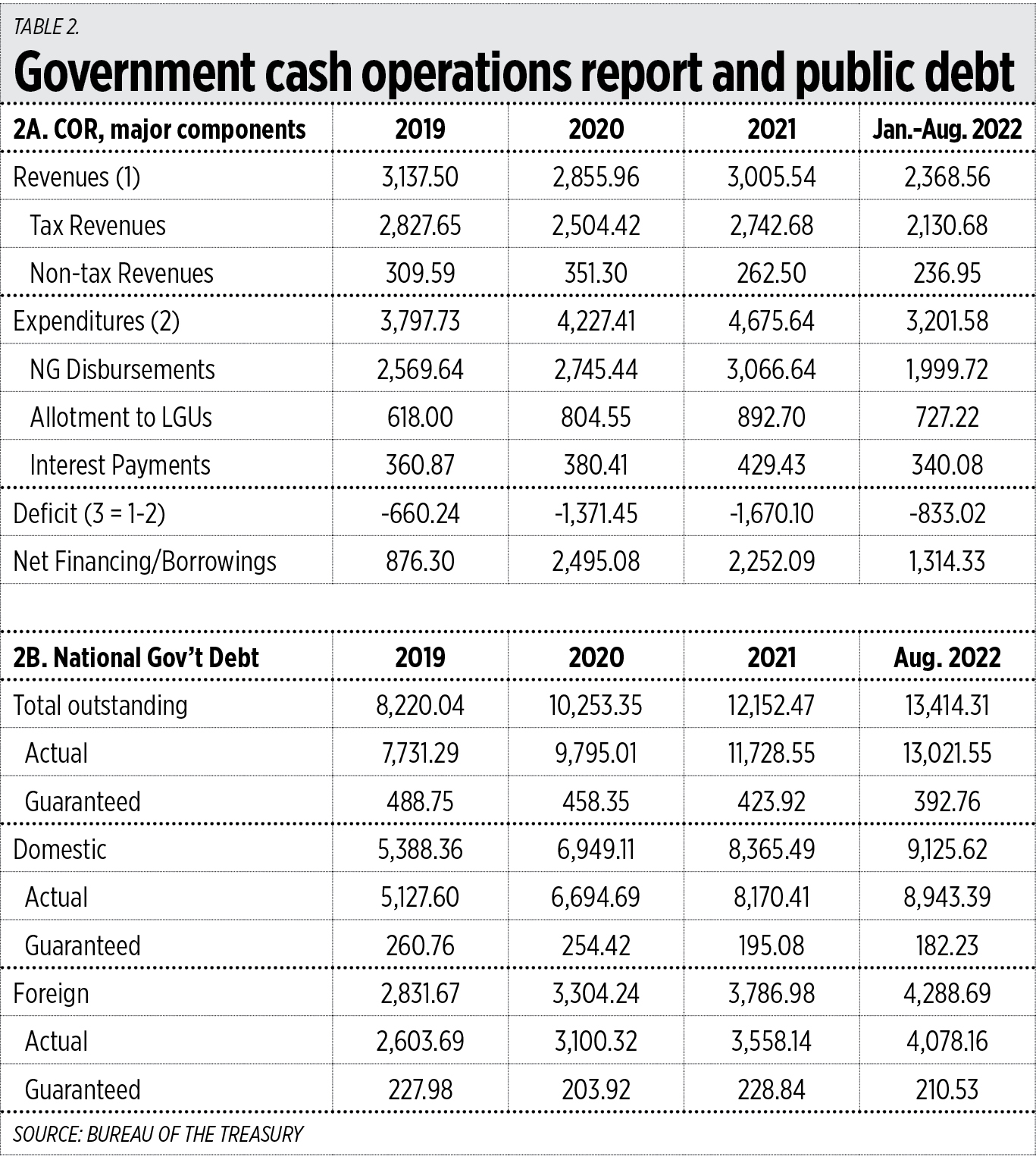

Last week, the Bureau of the Treasury released the National Government’s cash operations report (COR) and outstanding public debt. In the past two years, the budget deficits were P1.4 trillion and P1.7 trillion, while net financing or borrowings were P2.5 trillion and P2.2 trillion. From January-August 2022, financing has tamed to P1.3 trillion — hopefully it will not reach P2 trillion this year.

With high borrowings come high interest payments, P429 billion in 2021 and it might reach P500 billion this year.

The public debt stock has increased from P8.22 trillion in December 2019 to P13.41 in August 2022 (Table 2). It might reach P14.0 trillion by the end of this year.

The big challenge for the administration and the economic team is how to control the spending that leads to high borrowings and high interest payments. This can be done at least three ways.

One, reduce the size of many national agencies and let the local governments, which now have more funding under the Mandanas ruling, do more work. The Department of Budget and Management’s Bureaucracy Rightsizing program should materialize.

Two, reduce if not abolish old subsidies whenever new subsidies are created. The creation of a new welfare program is implicit admission that the old welfare programs are not working.

Three, reform and reduce certain entitlements like the huge military and uniformed personnel (MUP) pension. The pension of all retired civilian personnel in 2022 is P7.14 billion but the pension of MUP is P153.13 billion or 21.4 times larger than the former.

Comments

Post a Comment